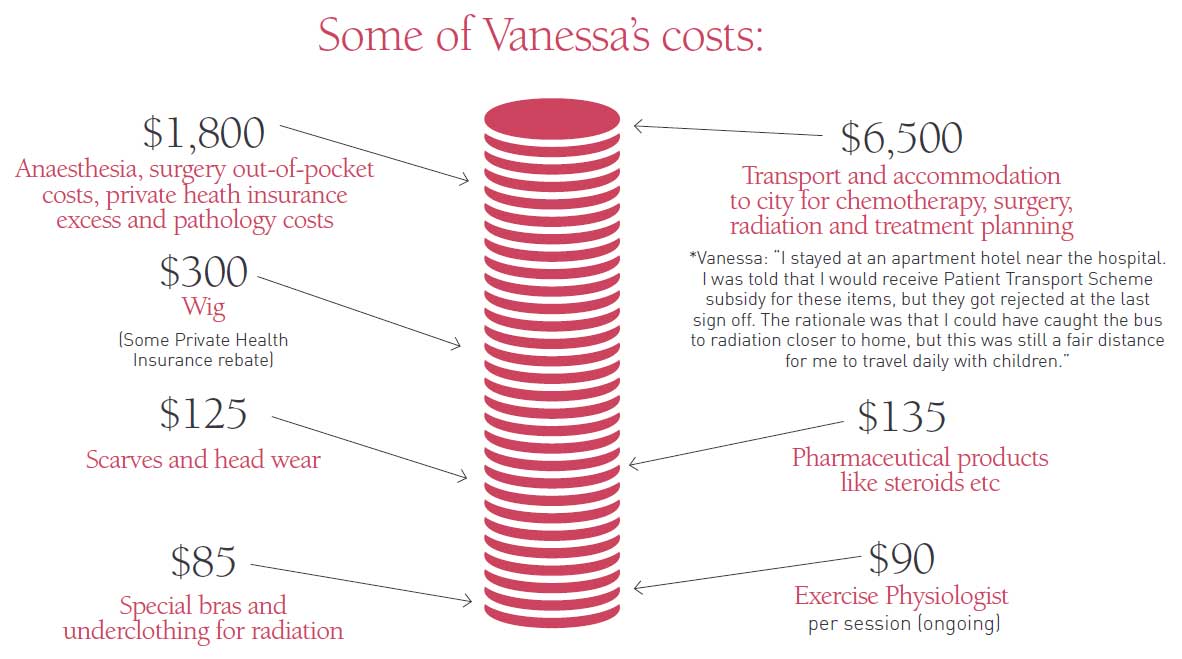

The out of pocket costs described by Vanessa on the previous page might seem hefty, but they’re all too familiar when it comes to breast cancer, according to senior financial planner Anne Graham. The Melbourne-based CEO of Story Wealth Management says a cancer diagnosis can be financially crippling to young and growing families, particularly when women are still working, raising children, contributing to mortgages and other household expenses, as well as managing busy lives. She says breast cancer is expensive, with a Deloitte report recognising that the average patient pays around $36,000 over a lifetime in out of pocket expenses – with most incurred in the first few years post-diagnosis.

“Obviously the out of pocket medical costs will vary patient to patient, depending on the treatment they have and whether they have private health insurance, Anne says.

“As a starting point, I would tell women to contact their private health insurance provider at the earliest opportunity after diagnosis and establish exactly what they are entitled to.

“I would then look at whether some of the treatments required might be able to be covered as a public patient, even for a patient who has private health cover.” It makes sense to get as much information as possible to enable you to make an informed decision.

A 2016 Breast Cancer Network Australia report noted that a woman with private health insurance will typically pay around double the out of pocket costs of a public patient.

This higher financial burden for private health insurance holders results from expenses incurred during surgeries, chemotherapy, radiotherapy, breast MRI scans and other diagnostic tests, as well as specialist consultations.

“But the other things that go under the radar and can be crippling to families are loss of expected income, for both patients and carers, as well as additional costs of ‘buying in’ help with household tasks and childcare,” Anne says.

“These are costs that are not actually related to medical expenses, but are part of the cost of cancer.”

And it might be all the ‘little things’ that really add up. A study by Cancer Council Victoria in 2016 estimated that the average cancer patient in Victoria would spend $1,128 on parking alone in their first year after a cancer diagnosis. Then there are costs of complementary therapies, wigs and turbans. Anne also warns that reconstructive surgery might be classed as elective if it is ‘after the fact’ and again, costs can blow out. “I would always advise women to do their homework and really investigate what they are going to be billed for.

“It’s also really helpful if they have another set of ears when this information is provided because there is so much that they are trying to process.”

Anne says there are a number of questions she would ask a woman upfront who had just been diagnosed with breast cancer in order to make a financial plan. These include:

How much do you have in the bank? Have you got access to money immediately?

Everyone should have a nest egg for situations like these. We typically say three months income or $10,000. But everyone’s expenses are different. It just provides you with an immediate buffer.

How much have you got in superannuation?

A woman who has been diagnosed with terminal disease and has a life expectancy of less than two years is able to get early access to their lumpsum benefits from their super fund, tax free. To do this, two medical practitioners must fill in documents noting that your life expectancy is less than two years. If you live longer, you are not obliged to repay the money and there is no penalty.

When breast cancer is not considered terminal, it is quite difficult to access superannuation early – and when we say early, we mean before age 55 at the earliest. You can access super these days for various treatments, but getting early release of super because you have breast cancer and need the money can be tricky. You need to demonstrate real financial hardship, but to do this you need to have been receiving an eligible Centrelink income support benefit for 26 continuous weeks to qualify.

A woman may be able to access her super under special provisions for a mortgage under difficult circumstances – when there is going to be a house foreclosure for example, but you can’t access it to pay rent. That’s just the way the rules are. If a woman is seeking access to super to pay for medical treatment, it needs to be signed off by a specialist, so it is quite a process.

And in the big picture, it is sometimes not the best thing to access super early. Depending on the prognosis, these funds might be better used later on. Have you got sick leave or annual leave accrued? Are you entitled to any time off work?

Even if a woman is planning to continue working through treatment there are going to be days that she will need to take off work, for treatment and/or the effects of treatment. It is important employers are flexible and patients are realistic about what they can achieve and manage. Having a frank conversation with an employer from the outset is important, so both parties are comfortable with how things are going to be managed. We find that even patients with resources behind them are reluctant to not work.

But I would also tell women to think about going part-time even in the short term, if it is not a financial necessity.

Can your partner afford to take time off work?

Women often need support at medical appointments and when they are recovering from the effects of treatment. If there is no other family support, a partner may need to take time off work to step in and help. We find women rely on family and friends a lot, through school communities and the kindergarten mums, things like that. The best of people comes through in times like this.

Can you approach your lender to ask for a freeze on payments for three months?

If you think you are going to be in real strife, you are better off being proactive. Sometimes lenders will allow a temporary freeze on mortgage payments and this might give you a bit of breathing space when some of the costs are rolling in. It’s always worth asking the question sooner than later, and before things get out of hand.

Are you covered by insurance?

I think trauma insurance is right up there with income protection insurance – everyone should have it. How much it costs depends on age, gender and even whether you are a smoker.

But the reality is that most women don’t have this kind of insurance in place, and don’t even know about it. People tend to begrudge paying for insurance, because they don’t see a return on investment. But there is very little to help women other than insurance when they face a breast cancer diagnosis.

Income protection insurance might cover you if you can’t work. A total and permanent disability insurance might be paid out if you can’t work again, but trauma cover has no relationship to your ability to work. What it is related to, is a diagnosis of a specified illness or injury. And the big ones that are typically covered under a trauma policy are heart attacks, stroke and cancer. It is a lump sum payment that is paid out on diagnosis. The beauty of a trauma insurance policy is that you get that paid provided the illness meets the definition in your policy. The lump sum payment can pay for treatment, or fill in the gaps when you have leave without pay, or your partner takes carer’s leave. It is money that can replace income or be used for treatment or even a holiday. It really can see people through some very tough times.

Anne Graham

* For more information about Story Wealth Management or to speak with a financial advisor, please go to www.storywealth.com.au or phone 03 8560 3188

This information is of a general nature only and has been provided without taking account of your objectives, financial situation or needs. Because of this, we recommend you consider, with or without the assistance of a financial adviser, whether the information is appropriate in light of your particular needs and circumstances. |